The system is also designed to make sure that the right valuers get to do the correct profile of jobs and to the correct standard. Here below are some of the features of the product that ensure this occurs first time, everytime.

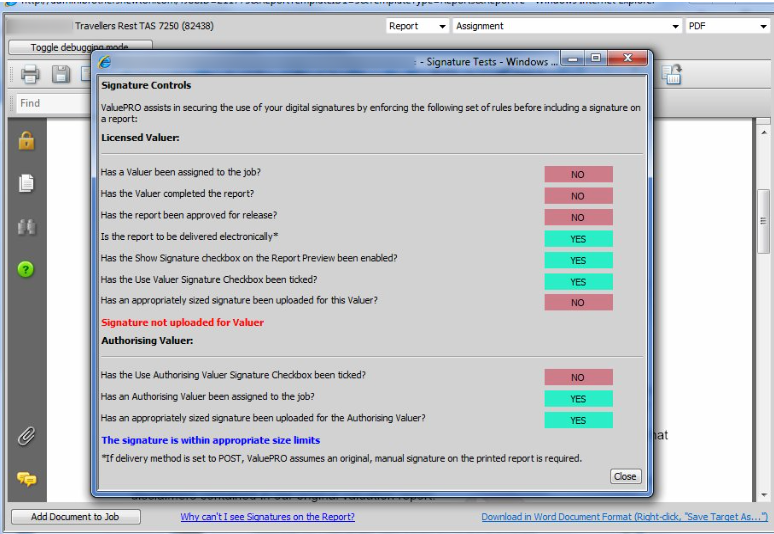

Securing the use of your Valuer's Digital Signatures

The product also stores electronic signatures of each valuer registered to work on the system. The signatures will only appear on a printed report is a series of strict rules have been adhered to.

The most common checklist of rules followed are summarised on this diagnostic screen that shows why this particular job will not show the valuer’s signature.

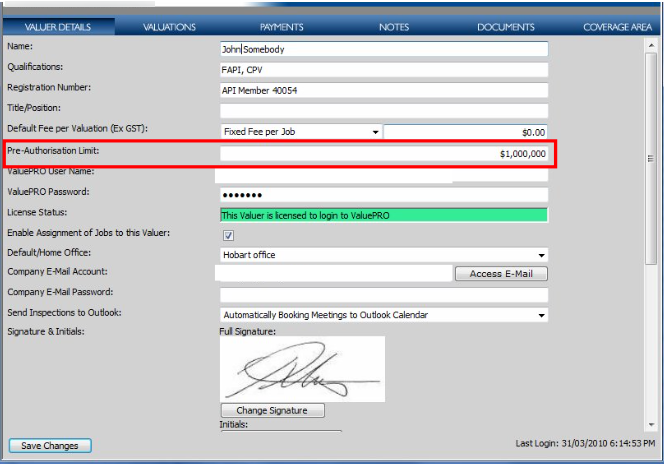

Valuer Restrictions and Approval Thresholds

Each Valuer can have a specific ceiling valuation limit set against their account. If a property is valued at or below this figure, the valuer is able to send a report back to the client directly from the system without having to escalate the job for approval by a senior valuer.

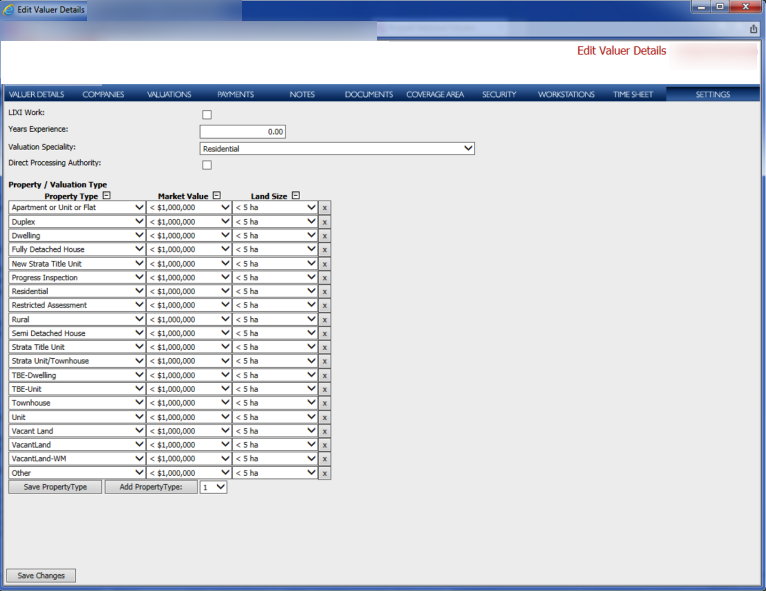

Valuer Competence Testing

You can also record specific business rules to determine a profile of valuation service types and property types that a given valuer is qualified and experienced enough to perform.

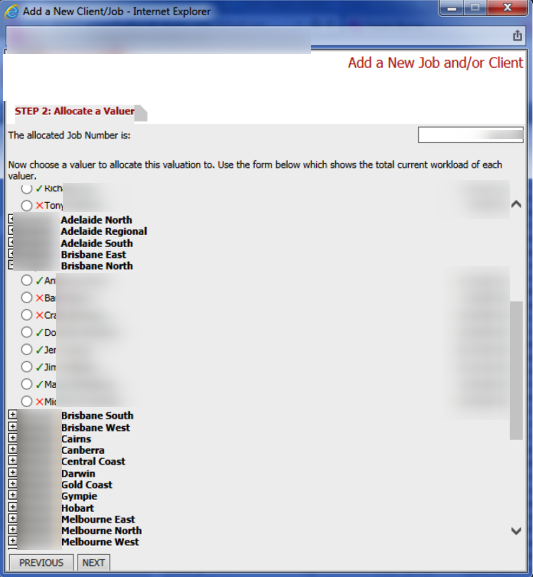

Valuer Allocation Safeguards

When a new job is being added, the administrative staff can see at a glance who within the organisation is appropriately qualified to perform this valuation. The system will permit a valuer allocation rule to be overriden by a master user - but will force that master user to record a valid reason for the override as well as tag that job to be auto-escalated for a senior valuer to review prior to transmission to the client.

Verification of Valuer’s work by AVM

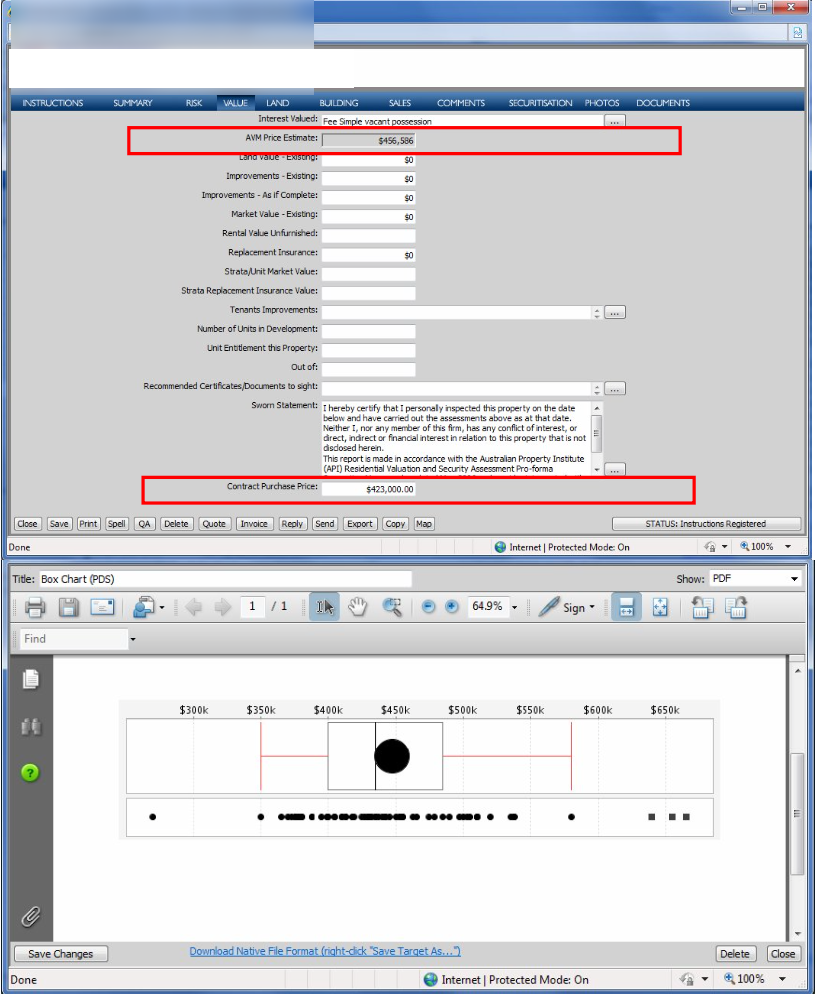

In addition to a valuation ceiling, the software can also optionally consult with industry accepted Automated Valuation Models (AVM) such as those offered by CoreLogic, PriceFinder/APM, Calnea etc... Using a combination of Hedonic modelling and various other well understood statistical techniques, the software is able to estimate, at the time of job registration, what the end valuation figure (and a high low range) may end up being. A confidence level score is also calculated to determine how reliable the AVM is likely to be.

The example above shows that the AVM believes the property is worth slightly more than the contract price that the purchaser of the property has signed for.

With this feature enabled, Valuers can also be assigned a percentage variation to AVM tolerance. For example, if a valuer has placed a value that is say greater than or less than 20% of the AVM’s figure, that the job should then be automatically escalated to a senior valuer for review and approval before release of the report to the client.

To avoid the valuer being influenced in their assessment in any way, the AVM figure can be hidden from their view when they access the job.

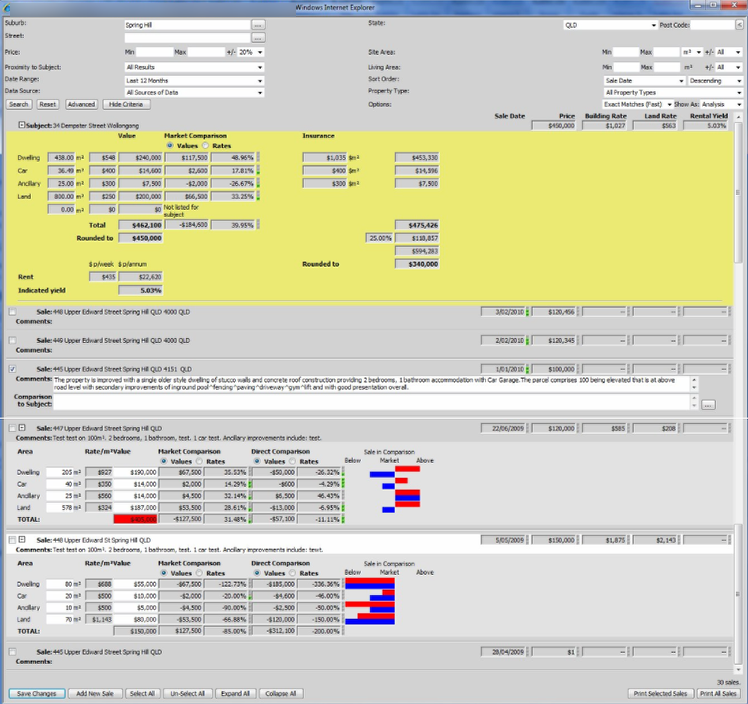

Market and Direct Comparison Rate Checks

Property valuation is well recognised to be equal parts qualitative and quantitative. Software tends to be most suited in the valuation process to assistance with the quantitative aspects.

There are 2 separate valuation methods that valuers use to attempt to capture both factors when valuing any property, namely:

- Market Comparison – compare the subject to property sales with similar attributes \L

- Direct Comparison – compare a sale to the subject based on a breakdown of the value attributed to each of the components \L

In the view shown above, the valuer is able to quickly compare on a single screen the full breakdown and analysis of each sale that matches their search criteria with the same breakdown for the subject property.

Various graphical indicators help the valuer to rank the degree of matching of a given sale in relevance to the subject property.

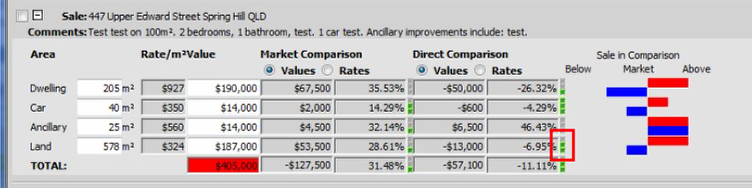

Confidence Level of Comparison Approaches

In this example the highlighted red square shows a “comparison Strength” indicator. As 2 out of 3 bars are highlighted in green, this indicates that the land component of this sale is very comparable to the land component of the subject property.

The Blue bar indicates that this sale’s attributed land value was also slightly below the market average for land within the sales included in the search results.

As more and more valuers working for a firm attribute sale value components in this manner, the usefulness of this data begins to grow. The resultant analysed rates start to form a collective peer review of valuations implicit in the process of assessing which sales evidence to select to support a valuation for the subject property.